Ethereum’s switch from a proof-of-work (PoW) consensus mechanism to proof-of-stake (PoS), via the much-awaited ETH 2.0 upgrade, is not here yet.

But as the platform slowly transitions, deposits into the staking contract on the Beacon Chain have risen continuously since November 2020. reached nearly 13 million ETH.

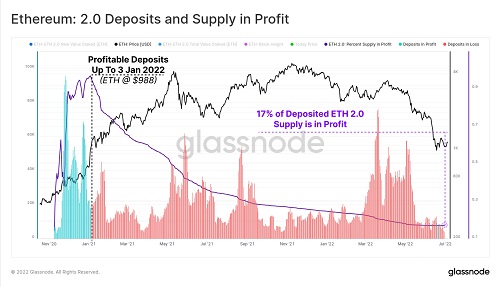

Most of the deposits happened before Ether’s price rose to its all-time high above $4,800. However, profitability for those coins has fallen sharply amid the bear market, according to analytics platform Glassnode.

Per a report the firm published on Wednesday, most stakers are “underwater” with only 17% of the staked coins are in profit at ETH/USD current levels of just above $1,100.

“Ethereum 2.0 stakers have deposited over 12.98M $ETH, with 62% of it flowing in before the Nov ATH. However, with $ETH prices collapsing over 78%, and coins unable to be withdrawn, only 17% of staked $ETH is now in profit.”

Chart showing percentage of ETH 2.0 deposits in profit.Source: Glassnode

Chart showing percentage of ETH 2.0 deposits in profit.Source: GlassnodeThe USD value of the deposited ETH has also fallen sharply, down from $39.7 billion at the November peak. Currently, that value is below $14 billion, reflecting a 65.2% decline.

No withdrawals yet

The ETH 2.0 deposits account for almost 11% of the cryptocurrency’s circulating supply.

Ethereum holders have continually deposited their coins into the Beacon Chain contract as they look to benefit from the rewards of running a validator. To do so, a staker needs to deposit 32 ETH, with solo staking as well as pool staking available.

But there is no withdrawal of staked ETH as yet. All that holders who bought and staked near the ATH can do is watch as the bear market wipes out their token’s value.

Notably, deposits into the ETH 2.0 contract have fallen in recent months. During the bull market, daily volumes ranged from 500 to 1,000 in 32 ETH deposits.

That has dropped significantly, with weekly averages now at around 122 per day.

The post Ethereum price watch: only 17% of staked ETH in profit appeared first on CoinJournal.